No Income, No Employment - NOT Hard Money!

Borrowers may choose between fixed- and adjustable-rate mortgages with terms from 1 to 30 years. Interest Only is available up to 75% LTV.

Why Get a No Income, No Employment Loan?

- Income documentation not required

- Income not stated or required

- Credit underwritten based on LTV, FICO, and liquidity

- Primary residence and second homes

- Asset seasoning 30 days

- Loan amounts up to $3 million

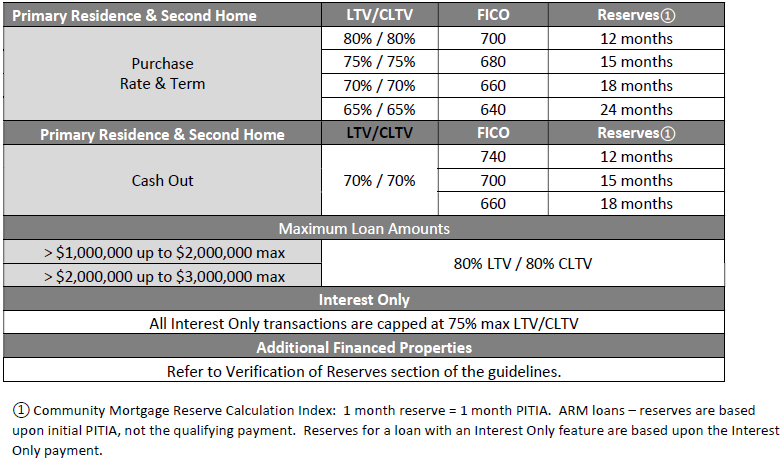

- LTV up to 80% purchase/rate-and-term

- LTV up to 70% cash-out

- FICO beginning at 640

- Debt consolidation = rate/term

- Available for purchase, refinance, or cash-out refinance

Ideal For?

- Self-Employed/Small Business Owner

- Volatile or Irregular Income

- Cannabis employment / ownership

- Retired (let's discuss this as sometimes a Fannie Mae loan could work for you)

- Seasonal & Gig Workers

- Real Estate Investors (investment properties NOT allowed)

- Owners & Employees of Cash Businesses

- Newly Self-Employed

- Transitioning from Recent Health, Family, or Other Life Events

- Looking to Tap Trapped Home Equity, but does not qualify conventionally

- Recent Immigration

- Disqualified Income

TIPS: Ideally, you want at least 30% down and over a 740 mid credit score for better pricing. Interest Only is available up to 75% LTV. There are origination / discount points, so let me talk to your Realtor about that and maybe asking for some seller credit to cover (this is not guaranteed). Impound / escrow account required. Cash out refinance seasoning is only 6 months, unless another cash out refinance was done within the last 12 months. Delayed Financing is available.

Income: Borrowers who meet the Community Mortgage eligibility requirements are not required to provide income documentation. Income is therefore not calculated nor stated on the loan application (1008/URLA), nor is a debt-to income ratio calculated as part of the programs established reasonable expectation of repayment.

Loan Documentation: Credit underwriting will often use “common sense” approach and use alternative and compensating forms of documentation to evaluate a reasonable expectation of repayment.

Character & Credit History: Credit underwriting seeks to understand a borrower’s character as part of the process. This can include reference letters, community activities, and reputation as well as credit history. Certain borrowers with limited FICO scores (e.g., new immigrants etc.) or with irrelevant or misleading FICO scores (e.g., identity theft etc.) may need more bespoke underwriting which considers alternative credit scoring and borrower character to evaluate the borrower’s reliability and reasonable expectation of repayment.

Borrower Eligibility:

1. U.S. Citizens - An individual who was born or naturalized as a citizen of the United States. Must have a valid Social Security Number.

2. Permanent Resident Aliens (Green Card) - An individual legally authorized to reside and work in the United States indefinitely. Legally authorized to reside and work in the United States indefinitely. Must have a valid Social Security Number AND a fully executed Certification of Resident Alien Status Form must be provided at the time of submission.

3. Non-Permanent Resident Aliens - An individual employed in the United States, but does not have a green card. Valid Social Security Number is required. The borrower's current visa must meet lender requirements and have a minimum of one year remaining prior to expiration. Visa types allowed: E-1, E-2, E-3, EB-5, G-1 through G-5, H-1B, L-1, NATO, O-1, R-1, & TN NAFTA

Ineligible Borrowers: Non-Occupant borrowers/co-borrowers,Any borrower suspended, debarred, or otherwise excluded per the LDP/GSA and/or OFAC/SAM findings, Diplomats, Diplomatic Immunity, Applicants with temporary protected status (i.e. DACA, Asylum), Irrevocable Trusts, Land Trusts,Limited or general partnerships (LLC), Corporations, S Corporations

Eligible Properties:

1. Primary Residences

2. Second Homes

- must be occupied by the borrower some portion of the year

- must be located a reasonable distance from the borrowers current residence

- restricted to one-unit dwellings

- the borrower must have exclusive control over the property

- must not be a rental property or a timeshare agreement

3. 1-4 Unit Residential Properties

4. Condominiums - Follow review process as required by Fannie Mae

- Fannie Mae warrantable up to max 70% LTV

- Detached Condos up to max 80% LTV

- Non-Warrantable up to 65% max LTV - Pending litigation will be considered on a case by case basis. Please provide paperwork regarding the litigation to Derek for review.

Ineligible Properties: Investment Properties, Condotels, Co-ops,Manufactured / Mobile Homes, Zoned Retail / Commercial, Log Homes, Properties that exceed 10 acres, Agriculturally / Rural Zoned Properties - Working farms, ranches or orchards

Appraisals: A Second Appraisal from an approved appraiser or AMC is required when the loan amount exceeds $1,500,000. When a second appraisal is provided, the transaction’s “Appraised Value” will be the lower of the two appraisals. The second appraisal must be from a different company and appraiser than the first appraisal (broker to order).

Appraisal Review: All appraisals require an acceptable, pre-closing, third-party desk appraisal review by an approved vendor in accordance with Appraisal Policy. If the Appraisal Review Product reflects a value more than 10% below the appraised value or cannot provide validation, the next option in the review waterfall must be followed. The next option would be either a field review or second appraisal, both must be from a different appraisal company and appraiser than the original appraisal. On transactions where the difference in appraised value is less than

10%, the acceptability of the appraisal is subject to UW Management review and discretion. The final appraised value is based on the lowest reported value amongst all of the appraisal documents/reviews.

Distressed / Declining Markets: If an appraiser identifies a property as “distressed”, it must be determined whether any deterioration is material and impactful to the overall value of said property. Properties located within a Declining Market as defined by the appraiser require a 5% reduction to the max LTV/CLTV offered.

Loan to Value (LTV): Purchase Transactions – LTV equals the lesser of the purchase price or appraised value. Refinance Transactions – If seasoned ownership is 12 months or greater, current appraised value is used. If the seasoned ownership is less than 12 months, use lesser of original purchase price or current appraised value.

Credit : Minimum credit score 640.

Tradeline Requireent - Two (2) tradelines reporting for 12+ months or one (1) tradeline reporting for 24+ months, all with activity in the last 90 days. At least one borrower must meet the tradeline requirement. *First Time Home Buyers are allowed to apply a 12 month recent and satisfactory VOR (verification of rent) towards the tradeline requirement. The following are not acceptable tradelines:

- "Non-traditional” credit as defined by Fannie Mae

- Any liabilities in deferment status

- Accounts discharged through bankruptcy

- Authorized user accounts

- Charge-offs or collection accounts

VOM (Verification of Mortgage): VOM required on refinance transactions only. If Primary is owned free and clear, no VOM is required. Mortgage being paid off through the transaction must be current, cannot be currently past due. 0 x 30 lates in last 12 months. All disclosed mortgage payment history is subject to review at Underwriter discretion. For VOMs tied to private mortgages – 12 months recent canceled checks and/or bank statements are required to support the VOM provided as well as a copy of the original Note plus any additional Riders or subsequent Modifications to ensure the loan being paid off is current and is not past its maturity date as that is considered being in default.

Required waiting periods after bankruptcy: Must be fully discharged, NO seasoning requirements. LOE required. Compensating documentation may be required at underwriter’s discretion.

Judgements: Must be paid at time of closing. Acceptable LOE (lettere of explanation) required.

Tax Liens: They will be found! Acceptable, proof of release. LOE required – compensating documentation may be required at underwriter’s discretion.

Collections: Acceptable, all open collections reporting in the most recent 48 months totaling more than $25,000 must be paid in full prior to or at closing. LOE required. Compensating documentation may be required at underwriter’s discretion. Medical collections not included.

Schedule of Real Estate Owned (REO): Initial URLA must reflect a complete Schedule of Real Estate for all properties owned by the Borrower. The property taxes, hazard insurance premium(s) and/or HOA dues (full PITIA) tied to any additional properties owned no longer require validation. Refer to the Verification of Reserves section to determine how to calculate the additional required reserves based on the total UPB of any mortgages tied to these additional financed properties.

Verification of Reserves: If the borrower owns additional financed properties in addition to the subject property the reserves must be calculated and documented as follows:

- 1.5% of the aggregate UPB of all mortgages tied to the additional financed properties.

- Reserves are calculated after considerations for required down payment. 100% value of stocks, bonds, mutual funds, 401k, retirement accounts and deferred compensation are acceptable sources of reserves.

- Must provide API data or most recent 1 month third-party statement in borrower’s name to meet reserves requirements.

- Documentation provided must, at minimum, validate the current month’s beginning balance, total deposits, total withdrawals, and current month’s ending balance. Assuming this required information is provided, all pages of the statements may not be required.

- Must provide source of funds for any recent significant deposits. A significant deposit is defined as 10% or more of the loan amount.

- Business funds are acceptable, must show proof of ownership.

- Business funds used to qualify are calculated based on the borrower’s percentage of ownership in the company. For example if a borrower owns 25% of the business then only 25% of the available balance of the account would be allowed to qualify.

- Gift funds are not acceptable for reserves.

- Cryptocurrency is not permitted.

- Cash out from transaction can be used to meet reserve requirement for refinances.

Verification of Down Payment:

- Must provide most recent 1 month third-party statement in borrower’s name to meet reserves requirements. Documentation provided must, at minimum, validate the current month’s beginning balance, total deposits, total withdrawals, and current month’s ending balance (one month full account statement as a pdf)

- Must provide source of funds for any recent significant deposits. A significant deposit is defined as 10% or more of the loan amount.

- Business funds are acceptable, must show proof of ownership. Business funds used to qualify are calculated based on the borrower’s percentage of ownership in the company. For example if a borrower owns 25% of the business then only 25% of the available balance of the account would be allowed to qualify.

- Cryptocurrency is not permitted.

- Assets held in foreign accounts may not be used as a source of funds to close or for reserves. These funds must be transferred to a U.S. banking institution account in the Borrower’s name and seasoned at least thirty (30) days prior to closing.

Gift Funds:

- Gift funds are acceptable for 100% or a portion of the down payment, principal pay down & closing costs, and require a gift letter with the givers name, address, relationship to borrower, amount and verify that the money is a gift and does not have to be repaid.

- Must document sufficient funds to cover the gift are either in the Donor’s account or have been transferred to the Borrower’s account or directly to the closing agent. Follow Fannie Mae requirements.

- Gifts of equity are not permitted

Seller Credit: Seller credit not to exceed 6% on purchase transactions.

Homeowner Education Class REQUIRED: Framework Online Homebuyer Course $75

Bottom line: If you don't qualify conventionally for a home loan, this could be your best option. This is not meant to be a long term loan for you. Ideally, you keep this a couple years or less and then refinance into a standard conventional or jumbo loan (example - you haven't done your taxes in a few years and you are self employed).